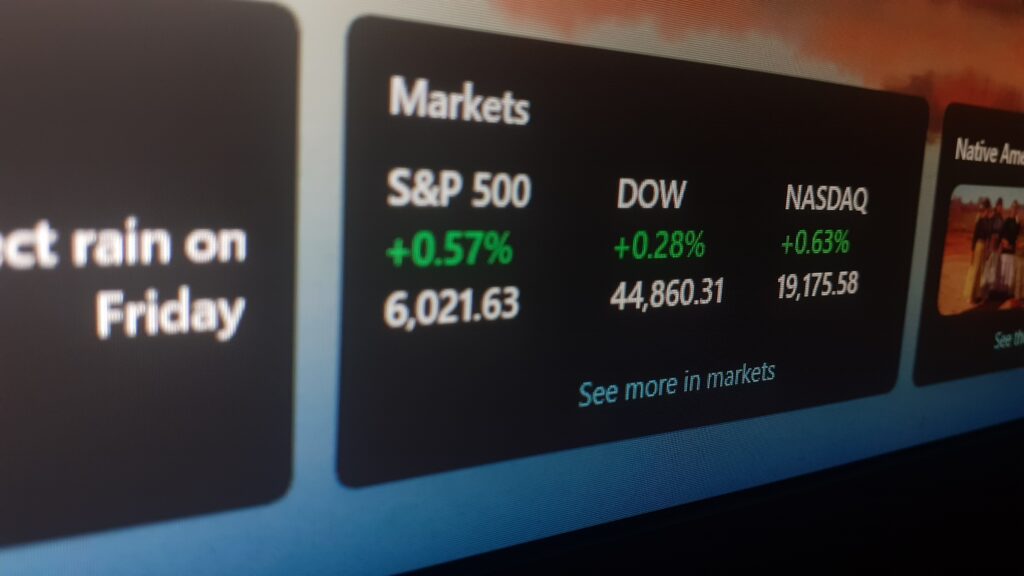

According to an analyst, Amazon.com stock remains a favorable investment after experiencing substantial gains this year. The analyst highlighted the company’s cloud business and retail sales performance as key factors for this positive outlook. On Tuesday, Seaport Research Partners analyst Aaron Kessler initiated coverage of Amazon (AMZN) with a Buy rating and a $145 price target. This price target suggests a 15% increase from the stock’s closing price on Monday. Notably, this bullish rating comes just before the report of the company’s earnings for it’s third-quarter. As of Tuesday, Amazon’s stock was up 0.8% to $127.59, reflecting a 52% surge in value this year. Kessler expressed confidence in Amazon Web Services, the company’s cloud computing platform for businesses, as a driving force behind his optimistic stance. Additionally, Kessler expects steady growth in e-commerce retail, particularly in essential categories such as beauty, health, and personal care. Despite consumers facing challenges from inflation and interest rates, Amazon continues to witness strong demand, although customers are increasingly focused on value when making purchases. Furthermore, Kessler anticipates advertising strength in 2024 as Prime Video plans to introduce advertisements. Subscribers will have the option to pay an extra $2.99 per month to enjoy an ad-free experience. “We estimate Advertising revenues of $45B/$52B in 2023/2024, representing growth of 19%/16%,” said Kessler. “Additionally, Amazon continues to introduce new ad offerings, and we are optimistic about the launch of Prime Video ads in early 2024, which should sustain solid advertising momentum.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.