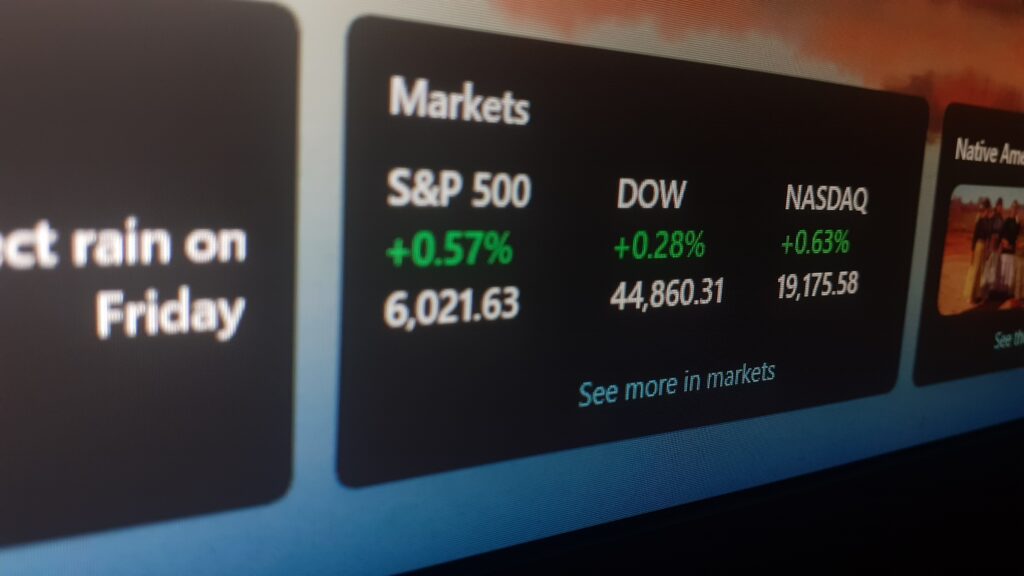

By all accounts, Apple reported possibly the best results from a technology company in this tumultuous earnings season. The company registered a beat on most of the financial metrics expectations from the sell-side analyst community. Second quarter earnings beat estimates, coming in at $1.52 versus an expected EPS of $1.42. Sales grew almost 9% year over year to top $97 billion versus the $94bn expected by analysts. Thanks to the large beats, 2Q22 became Apple’s largest non-holiday quarter in the company’s history.

Despite surging COVID cases in China, lockdowns across the country, and supply chain issues, the company produced stellar results. iPhone sales topped $50 billion, while services revenue almost hit $20bn for the quarter. Meanwhile, the company increased its new share buyback program to $90 billion and increased its quarterly dividend by 5% to 23¢/share up from 22¢.

Yet, the stock still traded down in the after-market hours as impact from supply constraints means that the company isn’t going to meet the strong demand for its products in the third, and possibly fourth fiscal quarters of 2022. In fact, Apple indicated that a lack of available parts, especially semiconductors, would cost between $4 to $8 billion in revenue for the third quarter. Based on the commentary provided, shortages in critical components will continue to be a near-term headwind, and Apple’s execution will become even more critical to its future success, than it was during the heights of the pandemic.

Furthermore, while supply constraints in the past meant that customers just defrayed their purchase, or waited longer for the delivery of goods, there are indications that competing products from the likes of Google, Samsung and others may start to entice those who do not wait to wish for over three to four weeks to receive their Apple products. Google’s recent Fitbit acquisition means that the company has started producing more integrated wearable and mobile phone devices, which could directly pull those on the fence about their next new device away from Apple.

There are also indications that Apple may want to raise prices in local currency in many geographic locations if the strong dollar maintains its gains. While inflation in other parts of the economy has meant rising costs for most products, phone manufacturers such as Samsung have thus far defrayed major price increases. This may have a dampening effect on the demand for Apple’s products, especially in emerging markets, where Apple’s market share lags that of its market share in developed markets such as the U.S. and Western Europe. iPhones are generally already 30 to 50 percent more expensive than competing products from other manufacturers in countries such as Indonesia and Brazil.

Lockdowns in China are also having an impact on demand in the region. However, Apple’s fortress balance sheet, its large buyback program and its stellar execution capabilities could counter potential softness in supply and demand issues amidst what could be a global macroeconomic slowdown. Additionally, the June quarter, which has traditionally been the slowest for the company, is possibly the best time for it to face supply constraints. Apple’s product roadmap and its rapidly growing services business also provides diversification and higher margin benefits which no other company in the world can match.

Apple’s broader ecosystem is enhanced by its services offerings, from Apple Music to the still relevant iTunes store. This revenue diversification will also help blunt any silicon part shortages that the iPhone and Apple Watch may face. Lastly, the company also remains an attractive value proposition. At roughly 26 times forward earnings, Apple is cheaper than many other technology companies. Its gross margin of over 40% is rare amongst companies that make physical goods, while its net income margin of above 25% is one of the highest of any large-cap company in the world. Though supply continues to lag, the situation should improve going forward now that nearly all of the company’s plants have restarted production. The large buyback would also serve to improve sentiment and provide a floor on the stock price going forward.