The rising dollar is disproportionately affecting the world economy. This increase of the strength of the dollar is thrusting the economy into further falloff as a result of higher cost of borrowing and a fuelling of instability in the financial markets, with no resolve in sight.

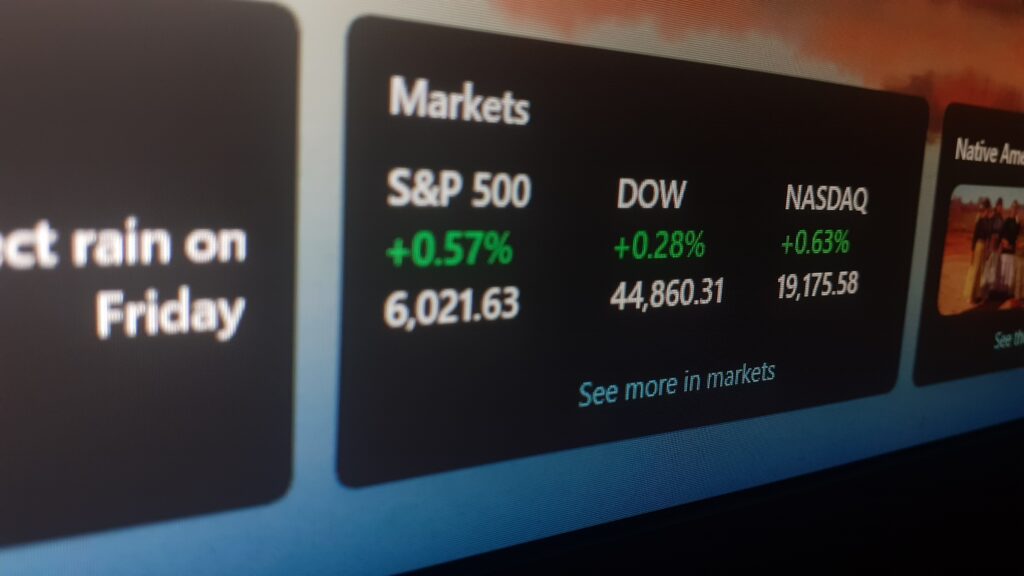

Due to the Fed’s stringent monetary policies aimed at controlling inflation by increasing interest rates, the US dollar has climbed to its highest since 2020, a whopping 7% escalation since the start of the year. Consequently, investors are flocking to purchase dollars as a safety net during economic turbulence.

A currency that is on the upswing is meant to help with the lowering of prices as well as assist the demand for imports by the US. However, there is a caveat to this in that it becomes costly for emerging markets to import, which then drives inflation rates and ultimately erodes their capital.

This in particular is a concern for foreign markets whose currencies have no choice but to either diminish, or they must intercept in an attempt to buffer the fall or increase their economy’s interest rates to strengthen their foreign exchange volumes. This month India and Malaysia had unexpected rate surges and India had entered the market for the purpose of strengthening its rate of exchange.

Developed economies are not exempt from these pitfalls either. Last week, the Euro dollar sank to the lowest it has been in 5 years; the Swiss franc is now on par with the US dollar- a phenomenon that occurred in 2019 and the Monetary Authority of Hong Kong utilized intervention tactics to protect its fixed exchange rate, while the Yen was at its lowest in 20 years.

These aggressive rate surges courtesy The Fed has set off a domino effect of capital flight and currency devaluation for global economies. However, there is a light at the end of this long and dark tunnel and will eventually be reached once the combined effects of plateaued growth and inflation in the US economy have materialized into a decelerated US dollar.

The issue that emerging markets face is a mismatch between currencies where governments and financial institutions have borrowed funds in US dollars but then loan it in their own currencies.

The IIF predicts that once the US economy contracts, China slows and Europe goes into a recession, the rate of growth on a global scale will come to a halt. The expectation according to economists is that growth in 2022 will be a fraction of what it was last year.

Amidst the global turbulence such as the Ukraine/Russian war and new covid lockdowns in China, investors are seeking financial shelter and those economies which are harbouring trade deficits are leaving open doors for greater instability.

The effects of heightened interest rates on both the sides of the Federal Reserve and the markets places developing economies in a risky position especially since the US has historically been a safety blanket for such economies. For example, last month saw a $4billion capital outflow from developing economies while there was currency devaluation and a 7% plunge of Asian bonds.

When the US coughs, the rest of the world catches a cold, and the tightening of the US monetary policies will have a ripple effect globally. Most economies external to the US are already in a disadvantageous position to the US.

Unfortunately, manufacturing companies like Toyota are experiencing the backlash. Operating profits have predicted a 20% decrease for the financial year even though yearly sales were strong. This was due to an unparalleled increase in raw materials and administrative costs and the yen is not expected to pull them out of this rut.

The Chinese Yuan has decreased, due to significant capital outflow, but it remains protected from the effects of the US dollar on the whole as local inflation rates are low and their monetary authorities can concentrate on sustaining economic growth because of this. However, the developing countries that depend on a strong yuan are being placed in a tenuous position. This chain of events can be attributed largely in part to China’s economic decline versus the stringent monetary policies of the Federal Reserve.

In progressive economies, devalued currencies create a complex policy issue for the European Central Bank, Bank of England and the Bank of Japan. A severely devalued euro is counterproductive to price stability strategies.

Waning currencies place additional strain on import prices which maintains inflation at a higher rate than the Central Bank’s goal of 2%. Monetary restrictions might relieve this issue in the short term, but the price of doing this is increased discomfort for local economies.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.