First things first, most major central banks are targeting inflation at about 2%. But when things turn rough, as they did during Covid, there are usually two go-to-trusted methods in most major central banks’ toolbox: lower interest rates and increase quantitative easing (i.e. buying spree of assets that increases balance sheets and injects digital money into the economy).

A year ago, the Federal Reserve did what has historically been done in Europe: cut interest rates close to zero, in this case, 0.25%.

Why? This is done to encourage lending by banks (read our previous in-depth article about the role of central banks here). Let’s take a brief look at what central banks have done to date, how effective it has been and how long can we expect them to hold on to these tactics.

Who is playing the negative charts?

So, why do a handful of central banks decide to go down the negative interest rate path?

As you’re most likely aware, negative interest rates don’t translate into everyday citizens taking out a mortgage and getting paid to do so. Negative interest rates are usually deployed to encourage investment into the local economy and increase the inflation rate.

The world’s leader in negative interest rates is Switzerland with -0.75% interest, and they have been holding this rate since 2015. But why? One of the key reasons is to keep the Swiss Franc from appreciating too much. The Swiss are also not afraid to intervene on the foreign exchange market if necessary. Inflation in Switzerland has been on a -0.7% for 5 years now. And ING expects the inflation rate to reach 0.5% by 2023, so there is unlikely much adjustment of the Swiss interest rate any time soon.

Who are the other negative interest rate players?

Japan currently sits at -0.1% and Denmark was the first nation to offer a negative interest rate in 2012. It’s currently close behind Switzerland with -0.5%.

And Denmark is a highly interesting case with banks having to ask many of their retail customers to contribute towards negative interest rates when depositing savings. There are increasingly serious concerns voiced that, although unlikely, there is a possibility that your everyday Dane could also be asked to contribute when depositing funds. Interest rates have started to turn into a highly political game.

Generally, there are serious questions raised about the effectiveness of negative interest rates. The main reason to deploy them is to encourage spending and investing. Yet, as the most recent kid on the negative interest block, Japan, has demonstrated, that strategy does not always pan out as intended. Japan’s lowering of the interest rate to -0.1% has done little to improve local spending and has caused serious issues with its bonds market.

The close to zero game

This could explain why many central banks have stuck to low or close to zero interest rates. The Bank of England has lowered its rate to 0.1%, the ECB is currently sitting at 0% and the Federal Reserve is hovering at 0.25%. And all have indicated, that they are unlikely to raise them any time soon. Some, such as the Bank of England, are not excluding the idea of negative rates.

Ultimately, it’s good to remember that central bank rates are rates that usually apply from the central bank to other banks. Low rates don’t necessarily translate to low mortgage rates or making finance more accessible.

And this is where fiscal policy can at times be more effective to encourage spending. Australia for instance has been known to hand out big lump-sum payments to all or certain tax residents when they want to boost spending at critical times.

Keeping on top of the interest rate games

The interest rate chatter on the great grapevine currently suggests that low interest rates are here to stay for a while, some say 2022, others expect them to last till 2023.

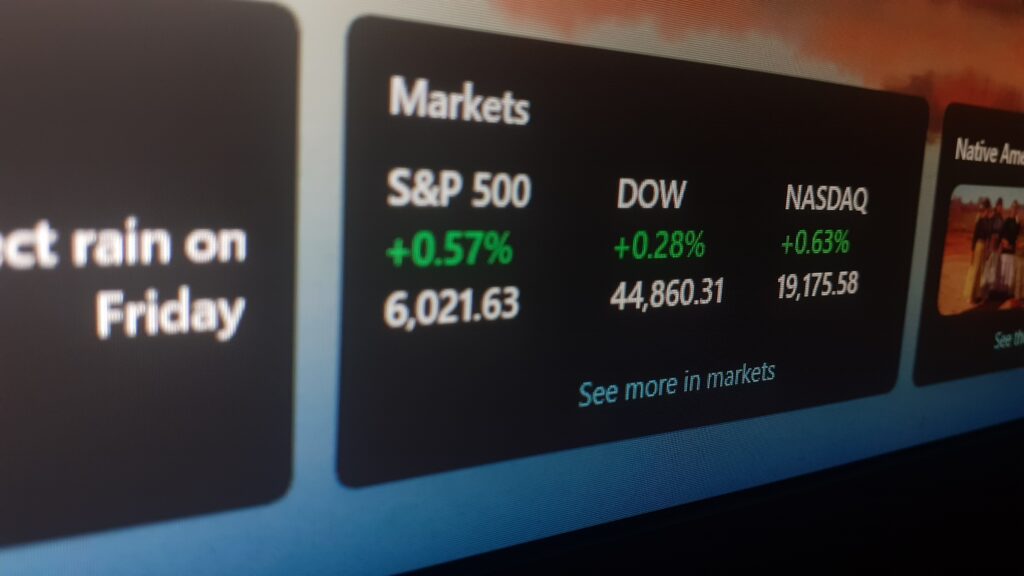

Remember, each time a board or body of a major central bank makes an announcement or if there’s a suggestion of interest rates moving up or down, the markets respond and it can be an interesting, but also a risky, time of volatility on the markets.