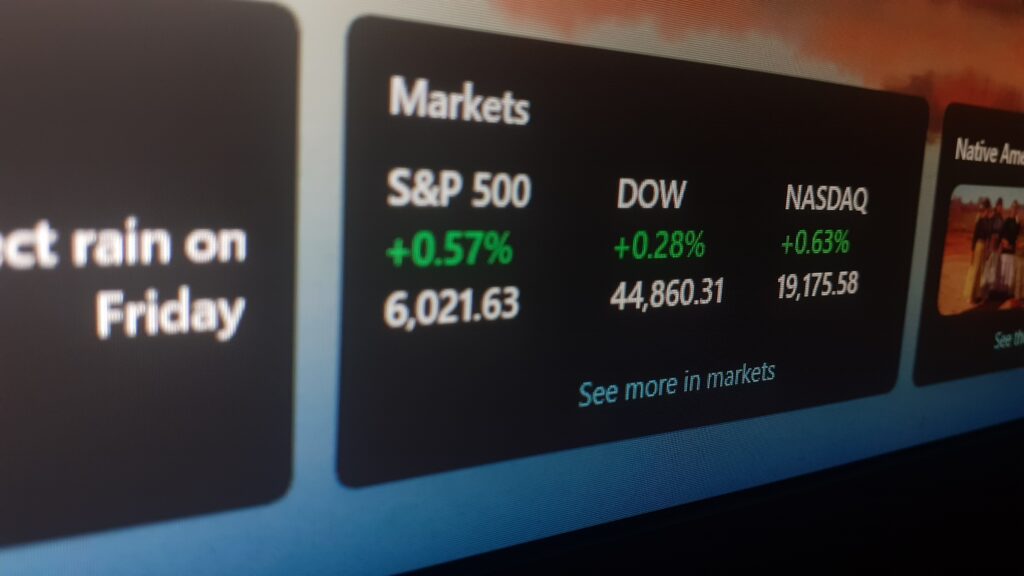

Ticker Symbol: LYFT

Lyft shares are surging, up 9% in the after-close market to $19, after reporting record earnings before interest, taxes, depreciation, and amortization that crushed expectations. The company’s shares had tanked in May after it reported its last earnings report. Shares are still down over 50% on a year-to-date basis, and well below the March 2019 initial public offering price of $72. Despite a difficult period during the pandemic, the company seems set to emerge from the pandemic with a more reasonable valuation.

The company posted second-quarter revenue which topped estimates, up 29.5% over the same period in 2021 to $990.7 million, versus the $985 million expected by analysts and the $975 million the company guided less than three months ago. Adjusted EBITDA for the quarter was $79.1 million, a record crushing the average analyst estimate of $18 million. EBITDA margins were 8%, much higher than the 1.8% modeled by the investors.

Additionally, active riders were up 15.9% year over year to 19.86 million while the estimate called for 19.8 million riders. Revenue per active rider jumped 11.8% year-over-year to $49.89, which similarly beat the consensus expectation of $49.65. The company reported a contribution profit of $590.5 million beating projections of $549 million as the contribution margin for the ride-sharing company jumped to 59.6% against the 56% expected.

Management said in the earnings call that ridership volumes are currently on track to exceed pre-COVID levels during the second half of the year as well. Chief Financial Officer Elaine Paul said in the earnings report that the firm remains confident in its ability to navigate through the tough macroeconomic headwinds to deliver strong results going forward.

However, the company’s third-quarter revenue forecast of $1.04 to $1.06 billion was shy of the average estimate of $1.12 billion. Further, Chief Executive Officer Logan Green said in the earnings call that EBITDA for the quarter would be between $55 and $65 million, lower than Wall Street’s projection of $67.4 million. The firm also noted that robust demand has outpaced the number of drivers on its app, but it sees the situation improving considerably in most of its markets.

Lyft’s strategic decision to focus purely on rideshare stands in contrast to its main competitor Uber’s decision to incorporate food and grocery delivery into its business model. Uber’s diversification has helped protect the top line from the effects of the Omicron variant to a much greater degree than Lyft. For example, Lyft’s revenue last year was still 11% shy of its 2019 figure, while Uber’s FY 2021 top-line was 34% higher than the figure recorded in 2019.

However, the focus on ridesharing has allowed the company to control research and development costs, while also allowing it to maintain a leaner organizational structure. Management had also previously noted that it would reduce its hiring for the foreseeable future as it looks to rein in its cash burn amid economic uncertainty.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.