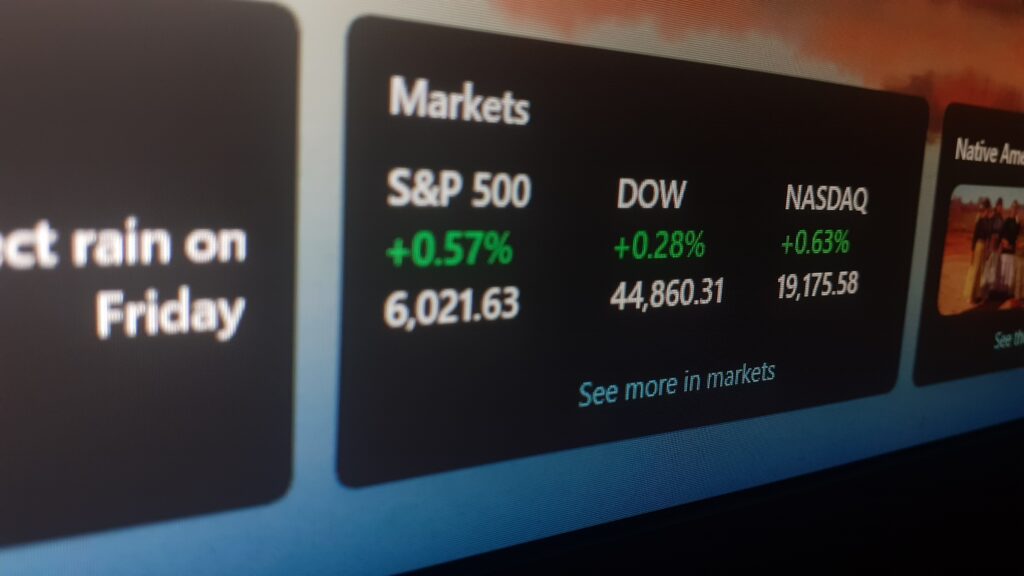

Ticker Symbol: PANW

Cybersecurity firm Palo Alto Networks reported strong fourth quarter results, and shares were trading up over 11% in the midmorning session as the company also issued strong forward guidance. Despite the carnage in the technology sector, Palo Alto has outperformed the S&P 500 for the year, with shares up 1.5%, versus the 13% decline in the benchmark. The Nasdaq 100, generally considered a gauge for the technology sector, is down over 20% in that same period.

Adjusted earnings per share for the fourth quarter came in at $2.39, versus the average analyst expectation of $2.27 and $1.60 from the year ago period. Billings rose a whopping 44% year-on-year to $2.7 billion, crushing the $2.35 billion expected by Wall Street. Product revenue was up 20% year-on-year to $408.1 million, ahead of the estimated $393 million. Meanwhile, subscription revenue disappointed slightly, but was still up 30% from 2021 to $1.14 billion. Estimates called for subscription revenue of $1.15 billion.

Perhaps most critically, the company reported that remaining performance obligations stood at $8.2 billion as of the July 31st, ahead of the average analyst expectation of $7.8 billion. Remaining performance obligations provides confidence in a company’s revenue pipeline and sustainability. Research and development costs came in below projected, up only 12% to $363.8 million versus the $380 million estimate. Adjusted gross margin and operating margin came in at 73.2% and 20.8%, respectively, for the quarter.

The company now sees adjusted earnings per share in the first quarter of fiscal 2023 to be between $2.03 and $2.06, against an analyst estimate of $2.04. It sees billings at $1.68 to $1.7 billion, while estimates called for $1.74 billion, and total revenue at a midpoint of $1.55 billion versus the anticipated $1.54 billion. For the full fiscal year, the company expects to earn $9.45 per share at the midpoint, against the average estimate of $9.28 per share. The company sees revenue between $6.85 billion and $6.9 billion, ahead of the estimated $6.75 billion.

The company expects the strong top-line growth to continue in the future given its capacity to execute, and strong industry trends. Hacking, corporate espionage and cyberattacks have become more common in recent years. Additionally, numerous U.S. government agencies have started requesting that companies across industries start amping up their technology and cybersecurity protocols to thwart state-sponsored spying and ransomware attacks.

Palo Alto Networks provides network security solutions, including firewalls that identify and control applications, scan content to stop threats, prevent data leakage, integrated application, user, and content visibility. Other companies in the sector were also rallying on the back of Palo Alto’s earnings. ZScaler, Okta, SentinelOne and Crowdstrike were all up at least 1.5% this morning, outperforming the Nasdaq which was roughly flat.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.