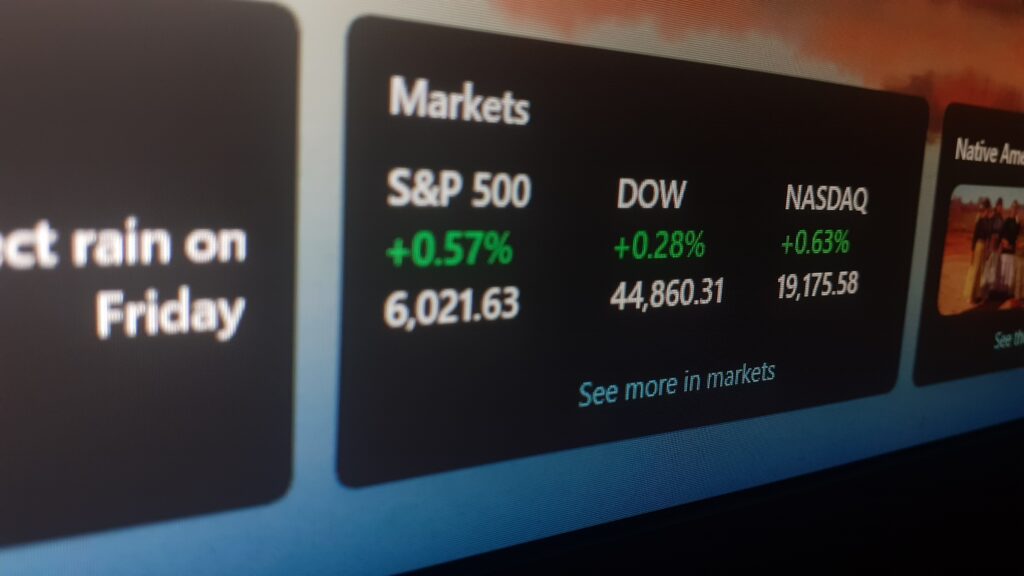

Ticker Symbol: NVDA

One of the largest chipmakers in the world, Nvidia, forecasted weak third quarter numbers which caused shares to slump by roughly 4% this morning. The company had provided forward guidance previously and the global economic slowdown was affecting its sales growth. Shares in Nvidia were down 41.4% for the year before the results were announced, reflecting the bearish investor sentiment in the technology space. The semiconductor manufacturer has underperformed the broader S&P 500 which is down roughly 13.5%.

Second quarter net revenue was up 3% year over year to $6.7 billion meeting the Wall Street consensus estimate. Data center revenue climbed 61% from the same period in 2021 to $3.81 billion. Gaming revenue, meanwhile, slumped by 33%, more than the average analysts forecast, to $2.04 billion. Automotive revenue, which is still in its infancy, was up 45% to $220 million. Professional Visualization revenue was down 4.4% to $496 million.

Furthermore, the company reported quarterly adjusted earnings per share of 51¢ which was ahead of consensus expectations of 50¢. Despite beating expectations, earnings were still down from the $1.04 per share reported in the second quarter of 2021. In the face of surging inflation and slowing revenue, the company also reported a gross margin of 45.9%, which was around 20 percentage points lower than its average gross margin over the past few years.

Management expects revenue for the third quarter to come in at $5.9 billion, plus or minus 2%. This was a big $1 billion miss on investor consensus estimate of $6.91 billion. Chief Executive Officer Jensen Huang said that declining demand for the company’s chips in gaming computers and challenging market conditions were the reasons for the lowered forecast. Investors have come to expect supercharged growth from Nvidia, which has consistently posted sales growth of over 30% over the past 3 years.

On a small positive, management indicated that gross margins in the third quarter would recover to 65%, higher than the 60.5% expected by analysts. Nvidia pre-ordered materials in the light of supply chain shortages, and as demand has cooled, it has more inventory on hand than it can sell without offering steep discounts. Huang said that the company is navigating supply chain “transitions” and that the firm would “get through” the challenging period. Nvidia still remains a darling of analysts however, with 37 buy ratings, 11 hold ratings, and only 1 sell rating, according to Bloomberg.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.