Monthly Market Summary

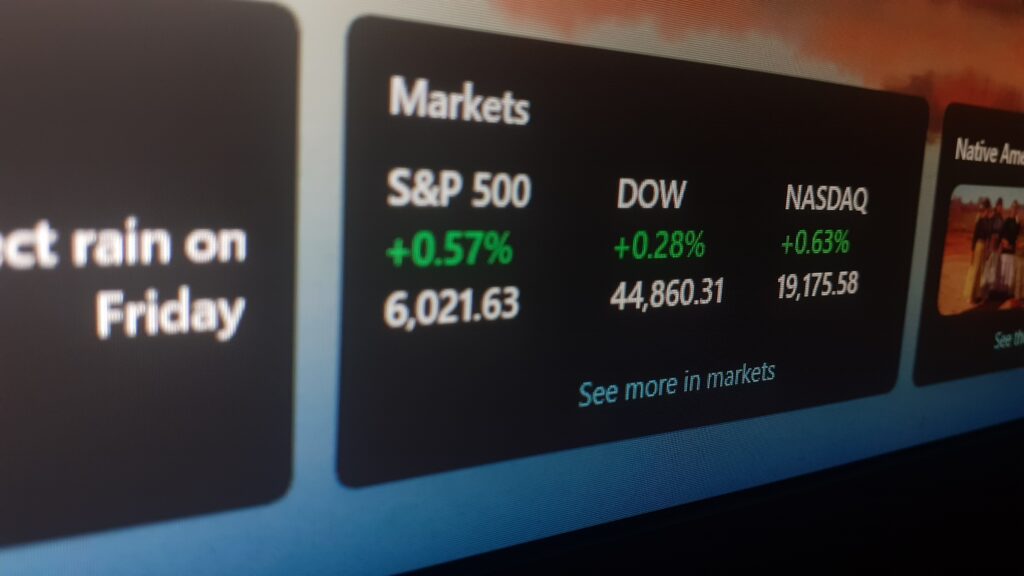

- The S&P 500 Index produced a -8.8% total return during April, outperforming the Russell 2000 Index’s -9.9% total return.

- Consumer Staples was the only S&P 500 sector to produce a positive return during April’s market selloff. Energy was the second-best performing sector as the price of crude oil traded around $100 per barrel. In contrast, the ‘Growth-style’ sectors, including Communication Services, Consumer Discretionary, and Technology, each traded more than -10% lower as interest rates soared higher.

- Corporate investment grade bonds generated a -6.7% total return, underperforming corporate high yield bonds’ -4.2% total return.

- The MSCI EAFE Index of global developed market stocks returned -6.7% during April, underperforming the MSCI Emerging Market Index’s -6.1% return.

Federal Reserve Policy Remains a Headwind for Equity & Credit Markets

April was another difficult month for both stock and bond markets. The S&P 500 Index traded -8.8% lower during the month, while the Bloomberg Bond U.S. Aggregate Index traded -3.8% lower.

Federal Reserve policy remains the driving force as the central bank raises interest rates and prepares to shrink its balance sheet to ease inflation pressures. It is a difficult and delicate balancing act to pull off.

Low interest rates and bond purchases stabilized the U.S. economy during the Covid pandemic, but removing the two pandemic-era monetary policies is proving to be enormously disruptive. Interest rates rose again during April as the 10-year U.S. Treasury yield surged +0.57% to 2.89%.

While 0.57% may seem small on an absolute level, it significantly impacts how investors position portfolios. Why? Interest rates represent the cost of money and are used as an input to value company shares. A higher Treasury yield offers investors a higher rate of return.

To incentivize investors to own riskier assets, such as stocks, the expected return must increase. Buying an asset, such as a house or stock, at a lower valuation should increase the expected return, which means the theoretical value of the asset should be lower as rates rise.

On a conceptual level, this is the messy valuation process the market is currently working through. It is trying to find the correct theoretical fair value of a company’s shares as interest rates rise. This is in addition to dealing with geopolitical tensions, new Covid lockdowns in China, and surging inflation.

What Can You Expect Moving Forward?

There is no easy answer or definitive path forward. This year’s selloff indicates some degree of tighter Federal Reserve policy is already priced into the market – we just do not know how much.

In addition, the list of market uncertainties remains long, including corporate earnings quality, economic strength, and the path of Federal Reserve interest rate hikes. Until the market receives clarity on these uncertainties, volatility is likely to remain elevated. The bumpy ride may not be done yet.