- Headline inflation surged to 9.1%, the highest since 1981, and core inflation came in at 5.9%. The readings were worse than what economists and market participants had expected.

- This may imply that the Fed will have to continue raising rates at an unprecedented pace to keep inflation in check.

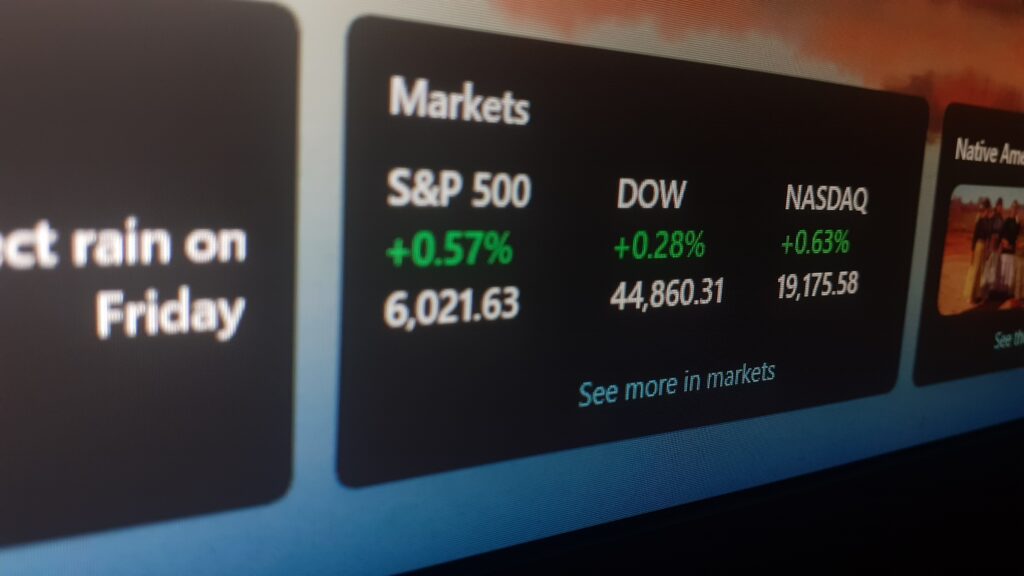

- Equity markets fell, bond yields rose, the U.S. dollar strengthened, and Bitcoin prices dropped after the report was released. Oil was down slightly.

- Rising prices, higher rates, a stronger dollar, and weakening demand are going to impact companies’ revenue and earnings growth. Valuation multiples may need to fall further.

- An inverted yield curve means that short-term rates are higher than long-term rates. This implies that the market expects a recession soon.

Inflation in the United States, as measured by the Consumer Price Index (CPI), advanced 9.1% from the year-earlier period in June. This was a new high after May’s reading of 8.6%. The number was more than analysts’ forecasts for the headline number to come in at 8.8%. Worryingly, core inflation, which is the headline number excluding volatile food and energy prices, also exceeded economists’ estimates, coming in at 5.9% versus the expected 5.7%, but was slightly below May’s 6%.

Market reaction to the news was swift with equities falling led by the Nasdaq down over 1%, the S&P 500 down 1.2% and yield on 2-year U.S. Treasury notes spiked by 12 basis points. The dollar also surged higher, and Bitcoin was off by 2%, once again falling below the key $20,000 level. The rise in the dollar now puts it at parity with the Euro for the first time since 2002, meaning that 1 Euro is now worth 1 U.S. dollar, down from 1 Euro being worth 1.14 U.S. dollars at the start of the year.

In the smallest bit of good news, oil prices were down slightly for the day and have fallen precipitously in the past month. West Texas Intermediate, the benchmark oil gauge in North America, was the last trading at $95 per barrel, down from $122 per barrel in early June. This may mean that the headline inflation for July could be lower than June reading especially as the price at the pump for consumers has dropped from a high of $5.10 per gallon in June to $4.75 per gallon currently.

While inflation was broad-based, there were areas where the spike in prices seems to be especially acute. As has been the theme for most of the year, fuel, shelter, food, electricity, used and new vehicle prices rose the most and were the largest contributors to the high inflation reading. Furthermore, a record 74.8% of the CPI basket is increasing in price at more than a 4% annualized basis, the broadest increase in prices the U.S. has ever experienced. Critically, real hourly earnings are declining as wage increases of roughly 5% can’t keep up with the 9% increase in prices for goods and services.

The report highlighted the specific areas where inflation has surged year over year: food at home was up 15%, transportation services up 29%, electricity up 16%, and shelter up 7%. With the Ukraine conflict keeping oil and gas prices high, China’s slow recovery from COVID lockdowns hurting supply chains, and an increase in labor costs, inflation could stay at an elevated level for a much more prolonged time than previously anticipated by policymakers.

Attention will now, therefore, turn squarely to the U.S. Federal Reserve System and the Federal Open Market Committee (FOMC) to see if the central bank would consider raising rates at an unexpected 100 basis points at its upcoming meeting in July. While the market was expecting a 50 basis points move in September before today’s report, the higher-than-expected headline inflation reading has shifted market expectations and futures are implying a much higher chance of a 75 basis points increase in September.

Based on today’s reading, investors are expecting the FOMC to raise its reference rate to 3.65% by the end of the year from the current reading of 1.75%. That could imply two 75 basis point moves in July and September, followed by 25 basis point moves in November and December. Additionally, market participants are increasingly expecting a recession in the short to medium term The yield curve is currently inverted, meaning that short-term rates are higher than long-term rates. The yield on 2-year Treasuries is roughly 15 basis points higher than the yield on 10-year Treasuries. Inverted yield curves are generally seen as a signal of an upcoming economic downturn.

Given that the figures this morning dash any hope that inflation may have peaked, higher expenditures could pressure Americans’ ability to withstand the cost-of-living adjustments. This, ultimately, means a more aggressive Fed, which could mean a weaker job market, lower retail spending, curtailed home buying, and higher borrowing costs. Although consumer spending has been strong in the face of inflation, retail spending could experience more pressure on a forward-looking basis as borrowing rates, especially on credit cards, increase.

For the stock market, a stronger dollar, higher interest rates, and weakening demand are a trifecta of negatives. The stronger dollar is going to result in translation losses for the largest U.S. companies which generate a hefty portion of their revenue from international markets. Higher interest rates generally result in higher financing costs and lower valuation multiples. And weakening demand may pressure top-line growth and surging prices could weaken operating margins further.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.